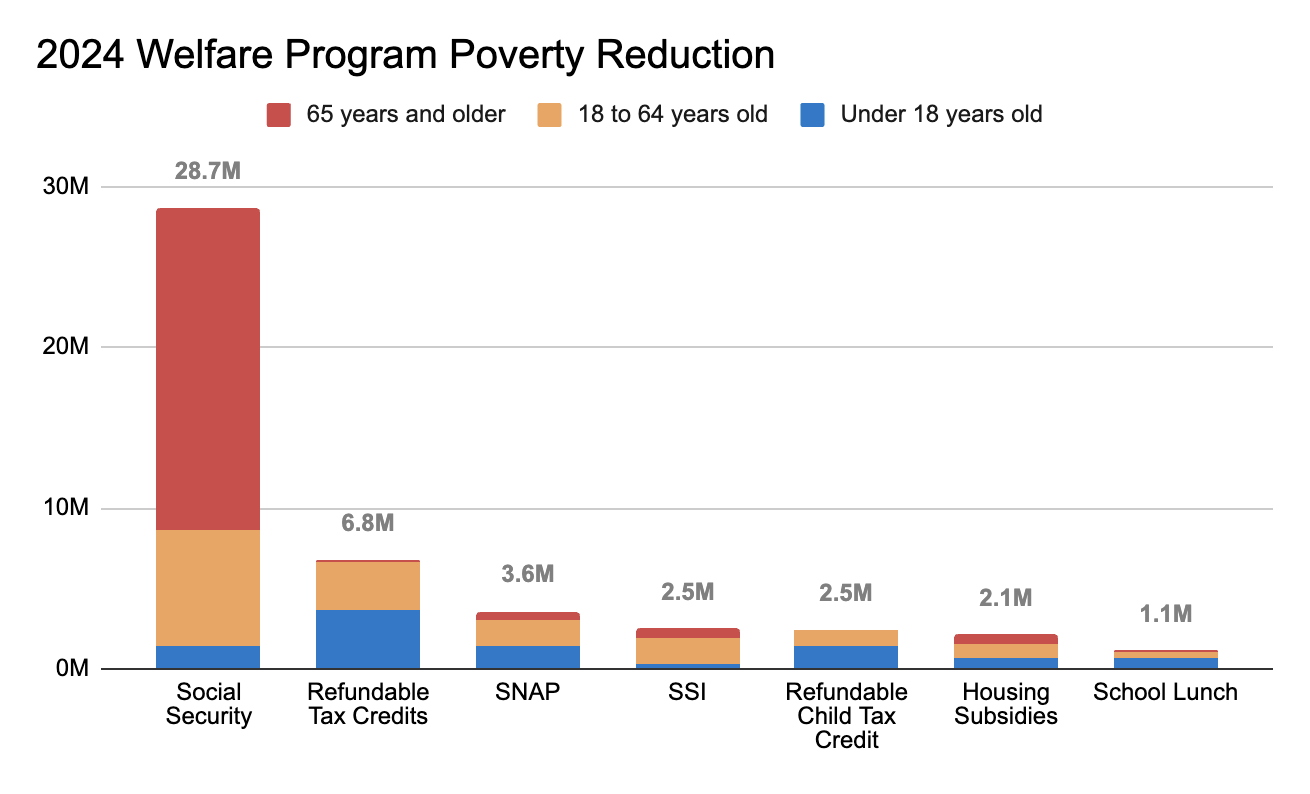

At Scioto Analysis, we frequently analyze poverty and the strategies designed to reduce it. One of the most common tools to combat poverty in the United States is welfare spending, or spending directed at needy families to alleviate poverty. While the efficiency and effectiveness of these programs are long-standing points of debate, research from the United States Census Bureau's 2024 Poverty in the United States report shows that year-over-year, welfare programs continue to reduce the number of people in poverty. The figure below shows the top seven federal programs in 2024 in terms of the total number of fewer people in poverty.

Welfare programs in the United States generally fall into two categories: cash assistance (direct payments) and in-kind benefits (direct goods or services like food, healthcare, or housing). We can also distinguish between how welfare programs are administered. Some programs are administered by state and local governments like Medicaid, Supplemental Nutrition Assistance Program, and Temporary Assistance for Needy Families. Others are tax-administered welfare programs, such as the Child Tax Credit and Earned Income Tax Credit, managed by the Internal Revenue Service.

Many policymakers favor in-kind welfare spending because it ostensibly allows policymakers to exert more control over use of funds by needy families. They hope this means household spending goes toward goods deemed necessities by policymakers and prevents use of funds on entertainment or other goods. A drawback of in-kind spending is that governments does not know the range of different needs felt at the household level and management of household budgets at the level of government leads to inefficiencies throughout the economy.

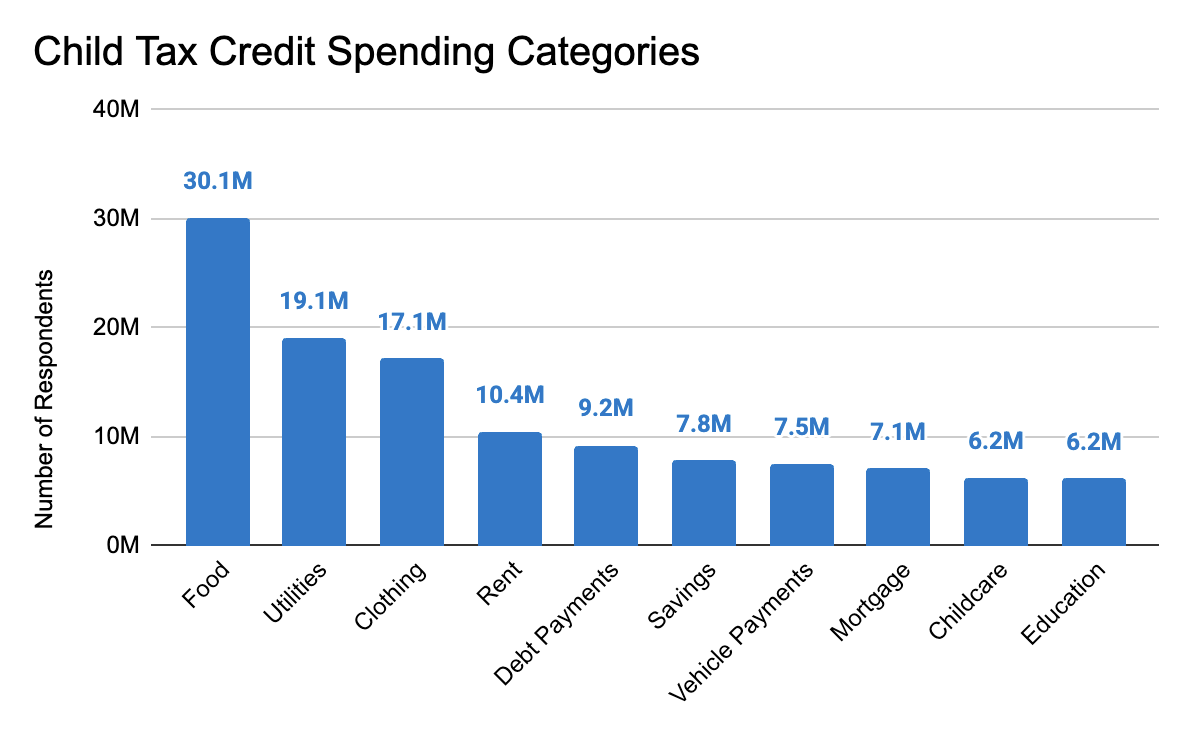

We can see this play out in how households spend cash when they receive it. In the chart below, U.S. Census Bureau data from 2021 shows that most recipients of the Child Tax Credit, a tax-administered cash assistance program, spend money on a range of goods. If Congress changed the cash transfer child tax credit to ten in-kind spending programs, it is unlikely it would be able to predict the amount of spending needed for these families in the correct quantities to achieve an efficient allocation of resources.

So, if direct cash payments are more efficient tools than in-kind benefits to alleviate poverty, why is a program like Temporary Assistance for Needy Families, which provides direct cash assistance to needy families in the United States, plagued with issues? The main answer is an issue of access. Over the past several years, Temporary Assistance for Needy Families has seen more stringent eligibility criteria, work requirements, and time limits. The goal of these policy changes is to improve participation in the labor force and help reduce reliance on welfare programs, but the actual result is a worsening of deep poverty rates.

A compelling underlying reason I see behind the ineffectiveness of TANF is the administration of the program. More focus is placed on regulating TANF than ensuring access. In addition, discrepancies between state and local government administration of TANF, along with many other welfare programs administered by state and local governments, means that poverty alleviation is starkly different state-to-state.

Another important consideration is scale. Since Temporary Assistance for Needy Families has been block granted and capped, the program is much smaller than other programs so does not help as many families as Supplemental Nutrition Assistance Program, the Earned Income Tax Credit, and the Child Tax Credit.

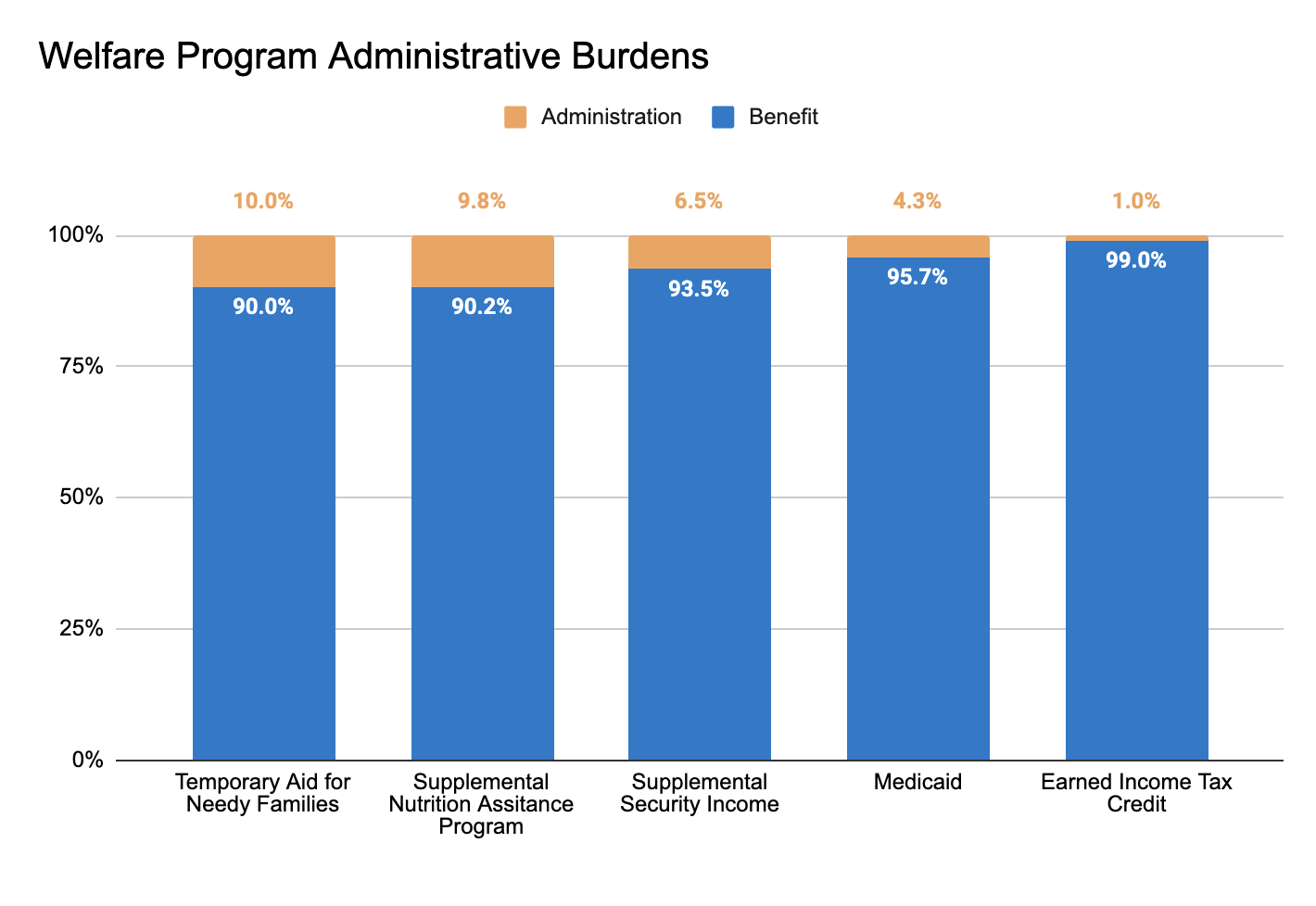

Using data from the Administration for Children and Families (2024), the U.S. Department of Agriculture (2023), the Supplemental Security Income annual report (2025), the Medicaid and CHIP Payment and Access Commission (2024), and the Congressional Research Service (2018), we can compare administrative costs as a proportion of total spending across different welfare programs. The chart below shows these administrative burdens for five selected welfare programs.

The original key takeaway from these numbers is that welfare programs are generally pretty efficient, with all programs spending 10% or less of their budgets on administration. The more interesting takeaway I see is how much more efficient the Earned Income Tax Credit program is than other forms of welfare. To be specific, the only two direct cash assistance programs shown in the chart are Temporary Assistance for Needy Families and the Earned Income Tax Credit, though Temporary Assistance for Needy Families also includes funds for other programs like job training and childcare. The proportion of funding for the Earned Income Tax Credit spent on administration is one-tenth the size of TANF’s. It could be the case that cash-based welfare programs administered through the tax code, like the Earned Income Tax Credit, avoid the bloat of state and locally administered programs, while also having stronger effects on poverty reduction.

Despite these statistics, the administrative benefits of welfare programs administered through the tax code may not be perfect. For instance, if we take into account the money that households spend on filing taxes to receive these kinds of benefits, the private administrative burden of receiving welfare increases. One study found that if we assume the tax filing fee to be 17.5% instead of 0%, the administrative burden of receiving Earned Income Tax Credit benefits increases to 11%. However, many households who receive the Earned Income Tax Credit are often eligible for free tax filing services, meaning that the real administrative burden to receive these benefits is likely somewhere in the middle.

In the 2024 tax season, the Internal Revenue Service introduced the IRS Direct File program, which ensured free tax filing services for filers with an adjusted gross income of $89,000 or less. The program has since been repealed, but it may be a worthwhile policy to keep administrative costs for programs like the Earned Income Tax Credit low while increasing accessibility for low- to moderate-income earners across the country.

One significant burden that tax-based welfare programs like the Earned Income Tax Credit can relieve is the benefits cliff. According to researchers at the Urban Institute, many earners who are near welfare cutoffs face higher marginal tax rates than some of the highest earners in the country. When accounting for taxes and reduced income from losing welfare benefits, marginal tax rates can easily reach 60% when households move toward full-time or gain a second earner. Tax-based welfare programs which reward people for working can help reduce these disparities.

Despite these advantages, there is still a significant gap in the efficiency of the welfare system in the United States. While tax-based cash assistance is a great tool for rewarding labor, the most disadvantaged households often fall through the cracks, either by not earning enough to require a tax filing or by not meeting work requirements set by welfare programs administered at the state and local levels.